We created this Georgia health insurance guide, including the FAQs below, to help you understand the health insurance options and possible financial assistance available for you and your family.

Georgia’s ACA Marketplace (exchange) is a platform where a variety of private health insurers offer health insurance for people who need to buy their own individual or family health coverage. This includes people who don’t qualify for Medicare or Medicaid, and also don’t have an offer of health insurance from an employer.

From 2014 through 2024, Georgia used the federally-run health insurance Marketplace, HealthCare.gov. But starting with the 2025 plan year – enrollments beginning in November 2024 – Georgia will have a state-run Marketplace, known as Georgia Access. 1 The federal government is working to transfer existing enrollees’ data from HealthCare.gov to Georgia Access. Enrollees will receive instructions ahead of open enrollment explaining how they can log into the new site, access their account, and renew or change their plan for 2025.

Depending on your income and other circumstances, you may be eligible for financial assistance that will reduce your monthly insurance premium (the amount you pay to enroll in the coverage) and possibly your out-of-pocket expenses . These subsidies are available through HealthCare.gov for 2024, and will be available through Georgia Access for 2025.

Hoping to improve your smile? Dental insurance may be a smart addition to your health coverage. Our guide explores dental coverage options in Georgia.

Learn about Georgia's Medicaid expansion, the state’s Medicaid enrollment and Medicaid eligibility.

Use our guide to learn about Medicare, Medicare Advantage, and Medigap coverage available in Georgia as well as the state’s Medicare supplement (Medigap) regulations.

Short-term health plans provide temporary health insurance for consumers who may find themselves without comprehensive coverage. Learn more about short-term plan availability in Georgia.

To enroll in private health coverage through the Marketplace in Georgia, you must: 2

Those are the only qualifications you need to meet in order to enroll in a Marketplace plan, but qualifying for financial assistance (premium subsidies and cost-sharing reductions) is a little different, and does have some additional parameters.

Eligibility for Marketplace financial assistance depends on your income and how it compares with the cost of the second-lowest-cost Silver plan in your area. In addition, to qualify for Marketplace financial assistance you must:

You can sign up for an ACA-compliant individual or family health plan in Georgia between November 1 and January 15. This is the annual open enrollment period.

(Note: As of late August 2024, the Georgia Office of the Commissioner of Insurance confirmed that the state had not yet finalized the end date for open enrollment for 2025 coverage. But it can’t be earlier than January 15, under the terms of new federal regulations that were finalized in 2024.)

For coverage to start on January 1, 2025, you must make your plan selection by December 16. 1

Georgia will no longer be using HealthCare.gov when people are enrolling in 2025 coverage. Instead, the Georgia Access platform will be used, with open enrollment beginning November 1, 2024.

After the annual open enrollment period ends, your opportunity to enroll or make a plan change will be limited. It’s generally only available if you experience a qualifying life event, such as giving birth or losing other health. But some people can enroll year-round even without a specific qualifying life event.

Enrollment in Georgia Medicaid and PeachCare for Kids (CHIP) is available year-round, so if you’re eligible for either of these programs, you can enroll anytime.

In Georgia, you can sign up for ACA Marketplace coverage through HealthCare.gov . This is the federally run Marketplace platform, and Georgia will continue to use it for all coverage effective in 2024.

But starting in the fall of 2024, for coverage effective in 2025, Georgia will be operating its own fully state-run exchange. Georgia had intended to make this transition in the fall of 2023, but the federal government pushed that out by a year. 5

To enroll in an ACA Marketplace plan in Georgia, you can:

You can reach HealthCare.gov’s call center by dialing 1-800-318-2596 (TTY: 1-855-889-4325). The call center is available 24 hours a day, seven days a week, but it’s closed on holidays.

You may find affordable health insurance options in Georgia by enrolling in a plan through HealthCare.gov – especially if you’re eligible for financial assistance. (Starting in November 2024, for coverage effective in 2025, enrollment will be completed through Georgia Access instead of HealthCare.gov.)

Income-based subsidies called Advance Premium Tax Credits (APTC) are available due to the Affordable Care Act. APTCs can help lower your premium payments each month, and most enrollees are eligible for these subsidies.

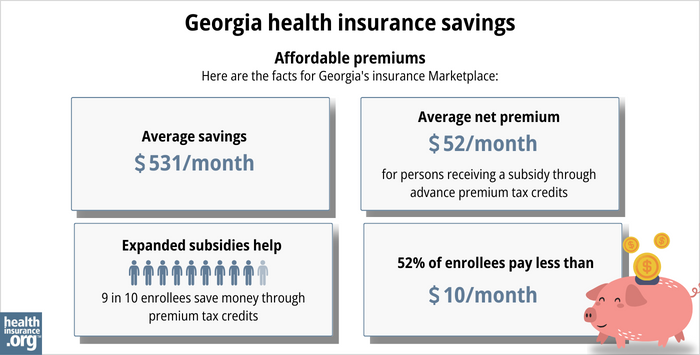

Ninety-six percent of the people with effectuated coverage through Georgia’s Marketplace in early 2024 were receiving premium subsidies. Those subsidies saved them an average of more than $531/month. After subsidies were applied, the average enrollee’s monthly cost (including those who paid full price) was about $69/month. 8

(Note that the numbers above are based on effectuated enrollment; the chart below shows some different metrics and uses data from all applications submitted during the 2024 open enrollment period.)

Although most Georgia Marketplace enrollees are eligible for premium subsidies, the state’s reinsurance program, which took effect in 2022, helps to keep premiums lower than they would otherwise be for people who aren’t subsidy-eligible. 10

If your household income isn’t more than 250% of the federal poverty level, you may also qualify for cost-sharing reductions (CSR), which are another type of ACA subsidy. These subsidies can lower your deductibles and out-of-pocket expenses as long as you select a Silver-level plan. Two-thirds of Georgia’s Marketplace enrollees were receiving CSR benefits as of 2024. 11

Depending on your income and circumstances, you may find that you’re eligible for free or low-cost health coverage through Medicaid or PeachCare for Kids (Georgia CHIP).

Georgia partially expanded Medicaid in mid-2023 (up to 100% of the poverty level) but imposed a work requirement for eligibility. This has significantly limited the number of people who are newly eligible for coverage under the program, which is called Georgia Pathways to Coverage. As of December 2023, only 2,344 people were enrolled in the Pathways program. 12 And by June 2024, enrollment had only grown to 4,318 people. 13

Learn more about whether you might meet the criteria for Medicaid in Georgia.

Nine private insurers offer health coverage through the Georgia exchange in 2024, with varying coverage areas. 14

All nine will continue to offer coverage in 2025 (ten if you count Anthem’s two separate entities). 15

There were eleven insurers in Georgia’s exchange in 2022, but Bright Health stopped offering coverage after the end of 2022. Friday Health Plans stopped offering coverage in the spring of 2023 and their existing policies terminated on July 31, 2023. 16

For 2025, Georgia’s Marketplace insurers have proposed the following average rate changes, 17 calculated before subsidies are applied. Rates are under review by state regulators and will be finalized before open enrollment begins in November 2024.

Average rate increases are for full-price plans, but 96% of Georgia Marketplace enrollees receive premium tax credits that help reduce their monthly payments. 8

Subsidy amounts change each year to keep pace with changes in the benchmark plan (the second-lowest-cost Silver plan) in each area. As a result of the American Rescue Plan , the subsidies are larger than they used to be, and available to more people. And this will continue to be the case through 2025, due to the Inflation Reduction Act .

If the cost of your current plan increases, you can explore other plans in the exchange that may be less expensive and offer similar benefits. Plan changes are possible during open enrollment, or with certain qualifying life events.

For perspective, here’s a summary of how average rates have changed over the years for Georgia’s ACA-compliant individual/family market:

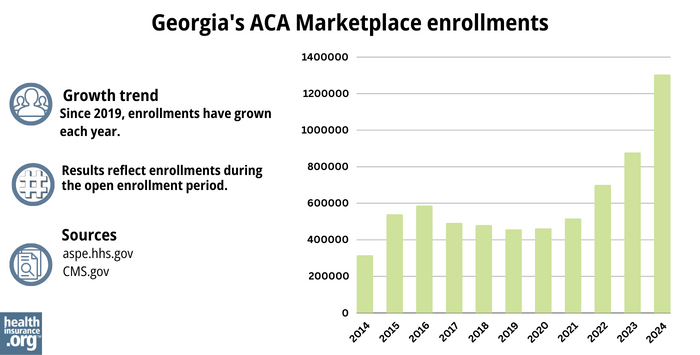

During the open enrollment period for 2024 coverage, 1,305,114 people enrolled in private plans through Georgia’s health insurance Marketplace. 28

That was a significant record high, and it came on the heels of the previous record high, when 879,084 people enrolled the year before, for 2023 coverage. 29

The chart below shows Georgia’s Marketplace enrollment over time. For several years, it hovered a little above or a little below 500,000 people, but has increased drastically in the last few years.

The increase is driven in large part by the enhanced premium subsidies created by the American Rescue Plan and the Inflation Reduction Act. And the additional enrollment growth for 2024 is also driven by the fact that people are once again being disenrolled from Medicaid, after that was paused for three years during the pandemic. CMS reported that by April 2024, more than 265,000 people who had been disenrolled from Georiga Medicaid had transitioned to Marketplace coverage. 30

Source: 2014, 31 2015, 32 2016, 33 2017, 34 2018, 35 2019, 36 2020, 37 2021, 38 2022, 39 2023, 40 2024 41

HealthCare.gov : The Marketplace in Georgia, where residents can enroll in individual/family health coverage and receive income-based subsidies. You can reach HealthCare.gov at 800-318-2596.

Georgia Access: The Marketplace in Georgia starting with 2025 plans (enrollment begins November 1, 2024).

Georgia Department of Community Health (DCH) – Administers Georgia Medicaid and PeachCare for Kids.

Georgia Office of Insurance and Safety Fire Commissioner – Regulates and licenses health insurance products sold in the state, as well as the brokers and agents who sell them.

Georgia SHIP – A resource for Medicare beneficiaries and their caregivers, providing counseling and assistance with various Medicare issues.

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written dozens of opinions and educational pieces about the Affordable Care Act for healthinsurance.org.